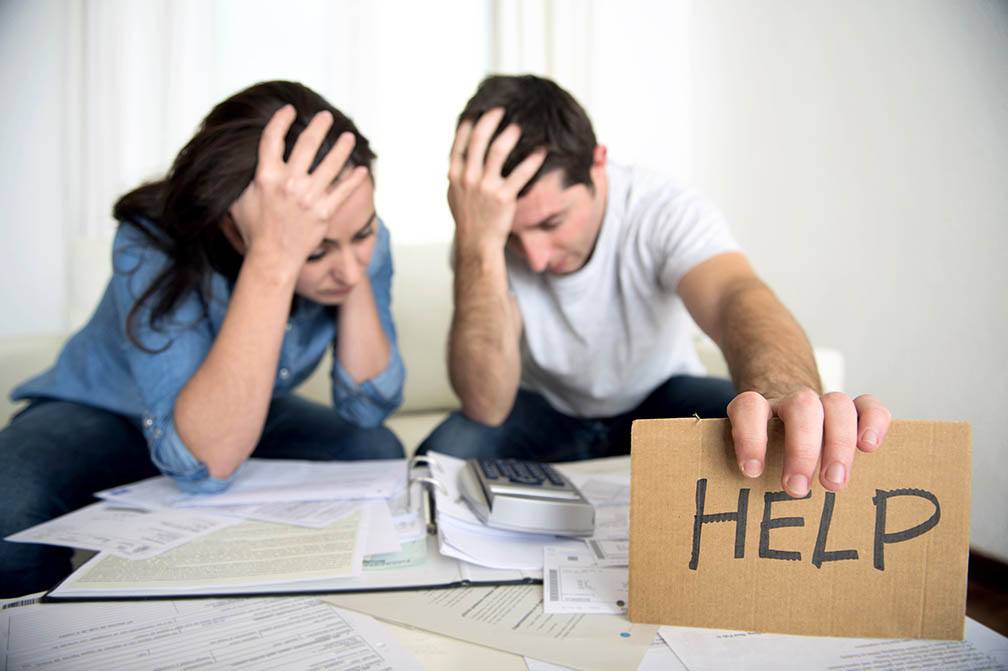

Current times are tough and there are a lot of homeowners who are having trouble making ends meet. Therefore, they are looking for ways to remain financially afloat as they assess their options. One option that people might have heard a lot about is called mortgage forbearance.

Current times are tough and there are a lot of homeowners who are having trouble making ends meet. Therefore, they are looking for ways to remain financially afloat as they assess their options. One option that people might have heard a lot about is called mortgage forbearance.

It is critical for everyone to understand what mortgage forbearance is and how this might be able to help them during these challenging times. Importantly, it is also important for people to know what mortgage forbearance is not.

What Does Mortgage Forbearance Do?

For those who are currently facing financial challenges, mortgage forbearance might be helpful. The goal of mortgage forbearance is to allow people to temporarily stop making payments toward their mortgage. This is particularly helpful when someone is looking for a new job or when families are struggling during a recession.

Depending on whether someone has a government loan or a private mortgage, their options for mortgage forbearance might be different. Therefore, it is critical for everyone to speak with their lender directly about mortgage forbearance before deciding this is the right option. Even if someone qualifies for mortgage forbearance, they still need to apply for it, as not everyone will be granted it. Otherwise, people risk becoming delinquent on their payments, which could lead to serious consequences.

Common Misconceptions About Mortgage Forbearance

It is also important for people to know what mortgage forbearance does not do. Even though mortgage forbearance will not hurt someone’s credit (as they will remain current on their loan), mortgage forbearance does not mean the mortgage is forgiven. It is possible that interest may accumulate on the loan when someone is not making payments, so this is critical to clarify. Or, it could take longer to pay off the loan. Finally, everyone who is applying for mortgage forbearance needs to understand how long this forbearance will last. Everyone has to make sure they know exactly when their monthly payments are going to resume.

Consider Using Mortgage Forbearance

Anyone who is having trouble keeping up with their mortgage payments should consider applying for mortgage forbearance. This can be a useful option for helping people stay in their homes without harming their credit scores or becoming delinquent on their loans.

If you are looking for a home, then you probably have a budget in mind. You also need to know about the most common factors that influence the price of a home. One factor that always seems to play a role in the price of a home is the quality of the school system. This makes sense. After all, a lot of people who are looking for a home have children (or are planning on having children) and want to make sure they have access to a quality education. At the same time, is it truly worth the price increase to have access to a better school district?

If you are looking for a home, then you probably have a budget in mind. You also need to know about the most common factors that influence the price of a home. One factor that always seems to play a role in the price of a home is the quality of the school system. This makes sense. After all, a lot of people who are looking for a home have children (or are planning on having children) and want to make sure they have access to a quality education. At the same time, is it truly worth the price increase to have access to a better school district? So – you’ve completed an initial mortgage pre-qualification and now you’re ready to take the next step and meet with your lender or mortgage advisor for the pre-approval interview. Are you ready?

So – you’ve completed an initial mortgage pre-qualification and now you’re ready to take the next step and meet with your lender or mortgage advisor for the pre-approval interview. Are you ready?